Long-term investment opportunities emerging from the chip shortage

At the moment, the world has a semiconductor problem. Consumer goods and auto manufacturers cannot get enough of them, causing disruptions in manufacturing their goods. The shortage is slowing economic recovery from the health pandemic and putting further hardship on the population. The semiconductor chip shortage has highlighted how vital the semiconductor supply chain is to the global economy as an essential component for manufacturing a whole range of required items for our everyday life. More importantly, it has highlighted the fragility of the manufacturing supply chain for semiconductors. At RC Global Funds Management, we look at how we got here, the consequences, and how we are playing the listed global equities market.

How did we get to the shortage?

Two significant events have created the chip shortage. Firstly, the US and China's escalating geopolitical tensions led to the US banning Chinese companies’ access to semiconductor technology. These companies responded by stockpiling semiconductors to avoid disruption to their manufacturing supply chain. Secondly, manufacturers’ miscalculation of the number of chips they required for manufacturing due to the unforeseen demand in response to the heath pandemic. The unexpected demand was driven by the need to replicate offices at home, more online home entertainment, and businesses beefing up their digital channels to increase market share or stay in business. These critical events have created the inflection point for the long-term driver of the shortage in manufacturing capacity for semiconductors.

The long-term driver for the shortage was the growing trend of fabless designers in semiconductor chips. Fabless designers design and maintain the semiconductor chip's intellectual property while their manufacturing is outsourced to fabrication companies called foundries. Since the early 2000s, this trend has gained momentum, as it meant less capital expenditure required for manufacturing facilities making it more economically beneficial for them. The leading fabless semiconductor chip designers are Apple, Advanced Micro Devices, Nvidia, and Qualcomm. The alternate approach is the Integrated Design Manufacturer, which does the design and manufacturing themselves. The advantage of this approach is maintaining all intellectual property from design to manufacturing. Intel is the flag bearer of this strategy, a winning strategy over many decades until recently, they have made missteps in manufacturing advanced microchips.

The long-term driver for the shortage was the growing trend of fabless designers in semiconductor chips. Fabless designers design and maintain the semiconductor chip's intellectual property while their manufacturing is outsourced to fabrication companies called foundries. Since the early 2000s, this trend has gained momentum, as it meant less capital expenditure required for manufacturing facilities making it more economically beneficial for them. The leading fabless semiconductor chip designers are Apple, Advanced Micro Devices, Nvidia, and Qualcomm. The alternate approach is the Integrated Design Manufacturer, which does the design and manufacturing themselves. The advantage of this approach is maintaining all intellectual property from design to manufacturing. Intel is the flag bearer of this strategy, a winning strategy over many decades until recently, they have made missteps in manufacturing advanced microchips.

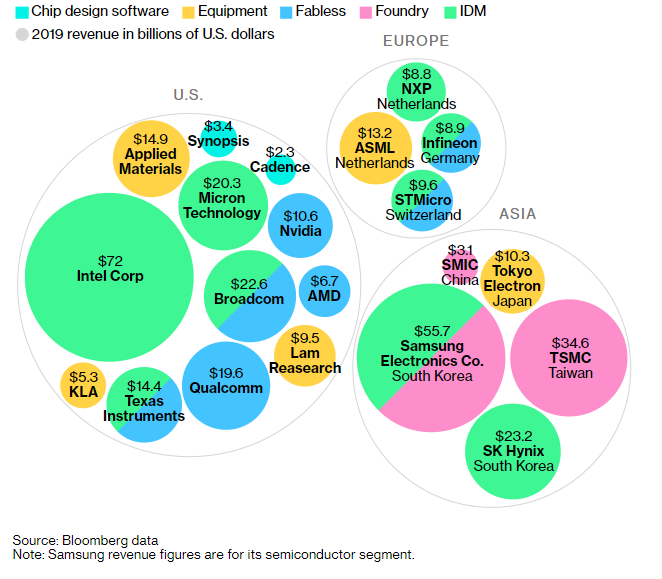

The growth in fabless designers, especially with the advanced microchips, is highlighted by Amazon and Google designing their chips for competitive advantage in the web services business. The rise of fabless designers has created two dominant suppliers in the foundry business Taiwan Semiconductor Manufacturing Company (TSMC) and Samsung Electronics , with the only other notable player being SMIC. To understand the concentration with the foundry business, the graph below provides an excellent illustration and the current landscape of the global supply chain for semiconductors.

The foundry business concentration has led to less flexibility in the supply chain for manufacturing chips because the available capacity for a fabless designer relies on the functional capacity the foundry business has built into their existing factories.

The consequences of the semiconductor shortage

The short-term consequences of the supply shortage have impacted the delivery of goods and services in the electronic and communication sectors. While at the same time, it has been a massive windfall for the players in the global supply chain for semiconductors. To highlight the demand level, TSMC fabrication facilities are running at 100% capacity to catch up with demand compared to regular peak times demand 80% utilization capacity.

The worst affected sector is the auto industry, which has stopped production in many plants because chips are unavailable to produce cars and led to billions of dollars in missed car sales. Typically automakers have enough inventory to avoid such critical disruption. However, their initial reaction to the health pandemic was to cut stock immediately, deemed appropriate at the initial phase of the crisis. However, the strong recovery through government stimulus has seen demand for cars outstrip supply. The best-prepared auto company was Toyota (a core holding of our Fund) , which always has a six-month stockpile of semiconductor chips on hand to handle a disruptive event. From the Fukushima disaster, Toyota learned a shortage in semiconductors chips is not an easy recovery. European and US automakers suffered the most, many of their plants had to halt production of the vehicles and workers stood down until they receive enough semiconductor chips to start production. The turnaround time for order new chips is about 26 weeks, which is not a short time and highlights the complexities in manufacturing semiconductor chips.

The complexities in manufacturing chips mean that shortage cannot be resolved with a flick of the switch and many analysts expect it could last till the end of the year Adding a new fabrication facility can take two to three years to complete and large amounts of capital, which is not tiny when considering it cost a minimum of $3 billion to build a fabrication facility at risk of becoming obsolete within five years.

The significant consequence of the semiconductor shortage was making competing nations realize how fragile the chips supply chain was with choke points in the manufacturing segment that could enable disruption to future economic prosperity and weaken national security. The US, China, and Eurozone countries led by Germany are competing to implement plans to remove the choke points by becoming more self-sufficient in manufacturing chips to protect themselves from geopolitical conflicts and strengthen national security. We are now going to see new fabrication facility being built in the US, China, and Europe away from the concentrated areas of Taiwan, Korea, and Japan. The government's actions to address these vulnerabilities are seen in their economic recovery plans from the pandemic. The Biden administration will allocate $50 billion from the Infrastructure Recovery Plan and maintain the CHIPS Act established under the Trump administration; a tool used against China in recent trade conflicts. Through their 14th five-year plan, China is focusing on research and development for advanced microchips, which is central to becoming a technology leader and counter US sanctions. Europe's pandemic recovery plan has allocated 30 billion Euros to provide incentives for new facilities in Europe to strengthen the auto industry's supply chain

The private sector has seized the opportunity with existing players making some big announcement. Intel will spend $20 billion on two new fabrication facilities in Arizona. TSCM has committed $100 million over the next three years to expand capacity, and Samsung $116 billion over the next decade to expand capacity. One of the more interesting announcements is Intel’s re-entry into the foundry business, where they are willing to supply competing fabless designers. Intel will run the new foundry business independently from the core part of the company.

Changing the landscape for manufacturing chips will see significant capital spending that should drive long-term growth for the supply chain of large foundry businesses. The supply chain includes advance materials, equipment makers, and service providers to build and optimize new fabrication facilities. Fabless designers will benefit with more choice in the foundry market and greater headroom for capacity. The greater choice in the foundry market should not be detrimental to existing foundry players, as they will be relied upon to deliver new manufacturing facilities in new locations and will receive incentives in doing so. Integrated Design Manufacturer will also benefit from the incentives when increasing their manufacturing capacity.

How are we playing shortage in the listed global equities market?

The semiconductor industry can be very cyclical where there are high demand periods with quick drop-off into low periods. These cyclical swings can create some volatility through the investment cycle when investing in the sector. At RC Global Funds Management, we use the volatility to find miss-priced opportunities in the listed global equities market. The essential nature of semiconductors for all things digital, electronic, and connected is a crucial attraction for us investing semiconductors segment, and we believe it will be a beneficiary of future demand driven by digital transformation, device connectivity, artificial intelligence, and mobility over the coming decades

In the short-term, the whole semiconductor sector benefits from the shortage in supply, which is reflected in the share price for global semiconductor companies that have risen significantly over the last six months with a 64% gain in the US semiconductor sector. It has only been in the previous month or two we have seen a pullback in the accelerated run-up that got a little overheated. To take advantage of the demand shortage, we initially focused on the number one player in foundry TSMC because of its strong market position with manufacturing advance micro semiconductors, strong balance sheet, and consistent return on equity. In the recent pullback, we made another purchase Qualcomm, a fabless designer and client of TSMC. Qualcomm gave us direct access to advanced chips required in smartphones and IoT connectivity, which benefits the rollout of 5G telecommunication networks worldwide and the megatrend of connectivity and mobility. One of the key characteristics we like was its exposure to supplying both the high-end and low-end smartphones giving us excellent exposure across the value chain, especially in the emerging markets where greater uptake of smartphones will occur.

A large amount of spend supported by the US, China, and European governments will create further investment opportunities in the listed global equities. We are focusing on companies that will benefit from the new landscape for foundries, and this includes the supply chains that will help them build, deliver, operate, and optimize these new fabrication facilities in the new regions. The increase in capacity and suppliers of fabrication will benefit fabless designers with more competitive options becoming available. It could also present future headwinds for TSMC and Samsung as more competitors enter the market, but the competitors will have to meet the high standards of delivery and customer service to compete successfully. To hedge against this headwind, we have taken a position in Intel, the world largest Integrated Design Manufacture in chips. Intel will be one of the new players entering the foundry business. In recent times, they have been underperforming due to their issues with manufacturing advanced microchips. The suppressed value of the share price has provided an opportunity to buy, as we believe the new management is correcting the manufacturing problems, and their new strategy entering the foundry business will be well supported by government initiatives. The two other purchases we made that will benefit from government support is Infineon and NXP. They are dominant chipmakers that supply the auto industry and provide good exposure to the auto industry moving to electric vehicles and self-driving.

We have to be aware of the risk of overbuilding capacity for fabrication through this period where demand does not fulfil the capacity and leaves the foundries and integrated design manufactures with under-utilized assets. The under-utilization will affect their return on deployed capital and reducing shareholder return over the long term. This potential headwind is very much at the investment teams thinking, as they have seen the downside with the oil and gas companies overspending in response to the commodity supercycle from growing Chinese demand in the early 2000s before the financial crisis.

Takeaway

The semiconductor shortage has been a big winner for semiconductor chip companies at the cost of other industries that cannot gain supply. The shortage has highlighted how essential semiconductors are in the supply chain for manufacturing consumer products and automobiles, validating the megatrend of digitalization, connectivity, and mobility that are driving long-term demand for chips. There is an excellent investment opportunity in foundries, foundries supply chain, fabless designers, and Integrated Design Manufacturers over the longer term. They will benefit from the growing demand for advanced microchips and accelerated government support with their pandemic recovery plan to guarantee future economic prosperity and national security. At RC Global Funds Management, we have already invested in the segment and are actively building our watch list for future opportunities, and we will keep you up to date with our future investments in this area.

Like what you're reading? Subscribe to our top insights.

Follow us on Linkedin.

3 Comments

-

Dave Austin 1 day ago

Dave Austin 1 day agoAs a Special Education teacher this resonates so well with me. Fighting with gen ed teachers to flatten for the students with learning disabilities. It also confirms some things for me in my writing.

Reply -

Christina Kray 2 days ago

Christina Kray 2 days agoSince our attention spans seem to be shrinking by the day — keeping it simple is more important than ever.

Reply

Post a comment

Like to organise a meeting

To discuss investing in our global managed equity funds.